Skip to content

1915

info@customs.gov.lk

Search for:

Top Bar

Search for:

1915

info@customs.gov.lk

Categories

Biodiversity Protection Detections

Consumer Protection Detections

Customs Detections

Narcotics Detections

Notices and Announcements

Sri Lanka Customs Achievements

Uncategorized

Recent Posts

The Customs House Agent (CHA) Certificate Course 2025 – III – Full Capacity

Results of the CHA Certificate Course Examination 2025-II

The Customs House Agent (CHA) Certificate Course 2025 – III

Phasing out of Fast Track and Green Channel

Sri Lanka Customs Launches Pilot Program on Paperless Submission of Customs Declarations

Primary Menu

Home

Personal

Travellers

Online Buyers

Crew Members

Business

Customs e-Registration

Authorized Economic Operator (AEO)

Registration Guide

Exporting Goods

Importing Goods

Bonded Operation

ASYHUB and ICT

ASYCUDA and ICT

Customs House Agents

Ship’s Agents

Trade Agreements

Customs Tariff and Tax Changes

Import Tariff

Classification of Goods

Time Release Study

Door-to-Door operations

Information

About Us

Overview

Directorates and Divisions

Customs Law

Feedback

Gallery

Museum

Detections

Contact Us

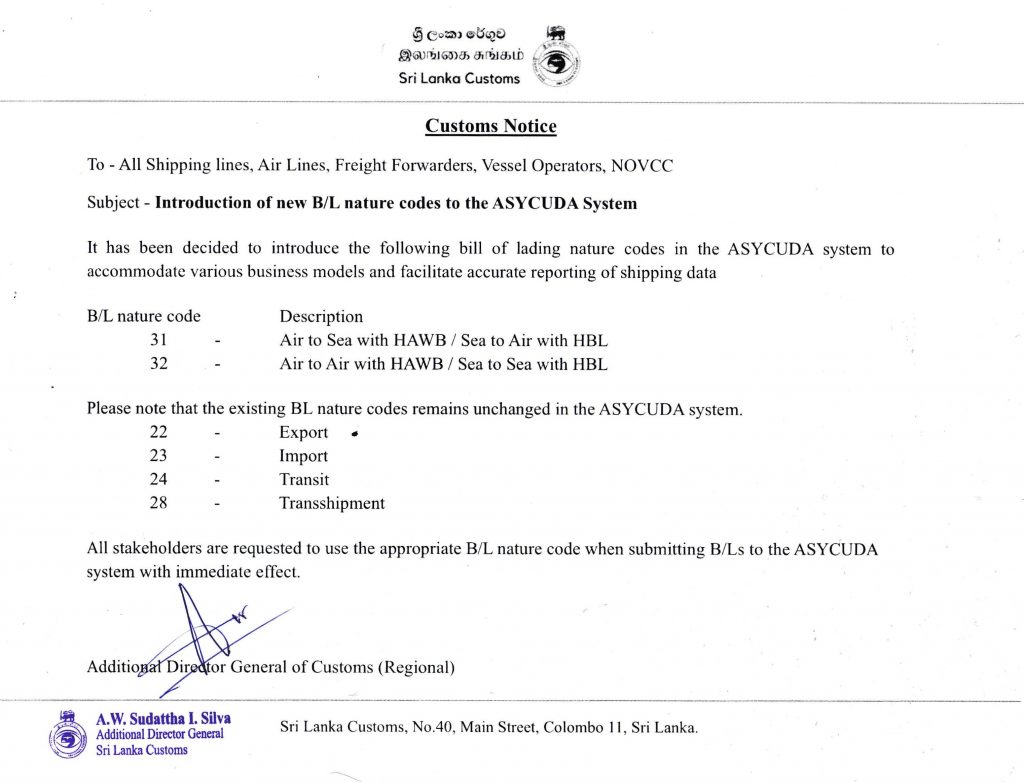

Introduction of new B/L nature codes to the ASYCUDA System

Sri Lanka Customs

>

Notices and Announcements

>

Introduction of new B/L nature codes to the ASYCUDA System

About the Author

admin

Post navigation

Procurement Notice: Building for Residential Accommodation for Duty Officers at Kankesanthurai Port Passenger Terminal

Mandatory Submission of Manifests via ASYHUB System – Effective from 07th May 2025

Search

Search for:

Categories

Biodiversity Protection Detections

(36)

Consumer Protection Detections

(12)

Customs Detections

(69)

Narcotics Detections

(22)

Notices and Announcements

(59)

Sri Lanka Customs Achievements

(1)

Uncategorized

(1)

You may also like these

The Customs House Agent (CHA) Certificate Course 2025 – III – Full Capacity

Results of the CHA Certificate Course Examination 2025-II

The Customs House Agent (CHA) Certificate Course 2025 – III

Phasing out of Fast Track and Green Channel